BART Should Have Been a Real Estate Developer

Commuter rail has a business model, we just never used it

Bay Area Rapid Transit (BART) is the San Francisco Bay Area’s most beloved commuter rail system.1 The service currently operates 50 stations in 28 cities across five counties. It’s long been a critical piece of transit infrastructure for the region, serving as the transportation backbone of the pre-covid economic expansion by connecting lower-cost East Bay neighborhoods to San Francisco’s commercial core.

BART, however, has seen better days. The system has suffered a 50% post-covid collapse in ridership, which has contributed to a $350 - $400 million hole in the annual budget. If voters don’t approve a sales tax measure in November, the agency will close as many as fifteen stations, reduce train frequency, and scale back hours of operation. That all may be necessary at this point, but I fear the cost-cutting will only reduce the system’s overall utility and accelerate its financial death spiral.

In moments of crisis, reflection is important. What I’d like to offer today isn’t a post-mortem of this specific budget shortfall, but rather a critique of BART’s “business model” as a whole. And while there’s a robust conversation to be had about the exorbitant cost of American mass transits — see the amazing Transit Costs Project — I want to draw attention to the other side of the ledger. Transit systems like BART create significant economic value; the problem is that they’re not allowed to recoup any of it. There is, however, a model for doing exactly this. And if we want to understand what fiscally sustainable commuter rail could look like, in the Bay Area or anywhere else, we need to appreciate how that model works.

How does BART make (and spend) money?

Before we get into how fixed-rail transit ought to be making money, we need to better understand how it spends it. Costs break down into two broad buckets: Operational costs, which cover everything associated with providing day-to-day service, and capital costs, which are necessary to build out and maintain the system’s infrastructure.

At its peak in 2018, BART covered 69% of its annual operating costs (~$685M) with ticket sales, which was quite good by American standards. The remaining 31% of its operational costs (~$308M) plus 100% of its capital costs (~$234M) were covered via funds from paid parking, sales taxes, parcel taxes, and grants from state and local government.2

One could be forgiven for thinking ticket sales ought to pay for everything.3 It’s the passengers who are getting value from the service, so the business model must be as simple as getting enough passengers to pay enough money to cover all the costs. After all, that’s how airlines work, right? As it turns out, the economics of commuter rail work differently. While it’s possible to pay for 100% of a system’s operating costs via ticket sales, it’s unheard of for those proceeds to also cover capital outlays.4

So what’s the alternative? For that, we head to Hong Kong to learn about the Rail + Property Development approach.

The Hong Kong Mass Transit Railway

Hong Kong’s Mass Transit Railway (MTR) is the city’s transportation backbone. The system opened in 1979 and, as of 2024, operates 167 stations. This system sees over 5 million daily trips and boasts an on-time rate of 99.9% (i.e., it’s basically never late).

Its financial performance, however, might be even more impressive than its operational metrics.

Though it varies by year, the MTR’s farebox recovery ratio has been as high as 187%. Read that again: The MTR can bring in nearly twice what it costs to run the trains based on ticket sales alone. But that’s just the rail part; the real money is in the property development half of the equation.

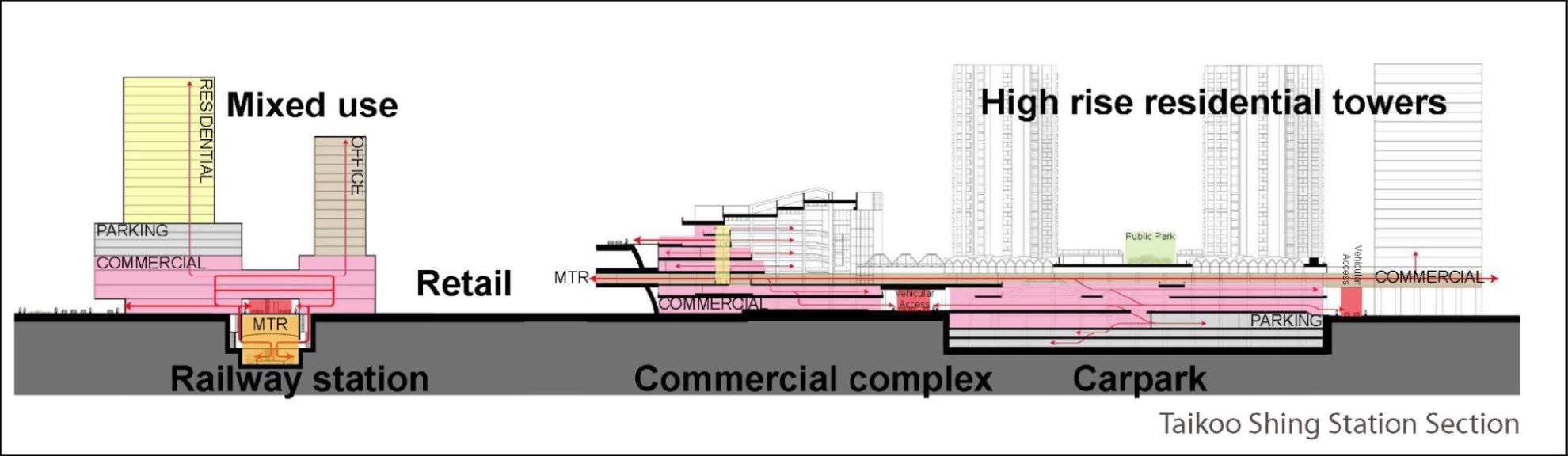

The other half of the MTR’s business is aggressively developing the land in and around each of its stations. More specifically, it monetizes its real estate position in three ways.

Developer payments: When MTR is granted development rights above a station, it runs a competitive tender, and the winning developer pays MTR a lump sum — essentially a land premium — before breaking ground. MTR pockets that upfront and walks away from the construction risk.

Retained investment properties: On marquee sites, MTR keeps a portion of the building for itself — the 18 floors it holds in Hong Kong’s IFC2 tower being the canonical example — and collects rent from tenants in perpetuity.

Station commercial businesses: MTR operates or leases the shops, restaurants, and retail concessions inside the stations themselves.

Together, these three streams — one-time developer payments, long-term rental income from retained floors, and in-station retail — generate roughly $1.3 billion USD in annual property profit that funds MTR’s capital program. It is, in other words, a transit agency that finances its own expansion by acting simultaneously as a land developer, a landlord, and a mall operator.

The economics here are quite circular.5 The rail line makes the surrounding real estate more valuable to develop. That development enables more people to live and work near its stations (roughly 43% of Hong Kong’s workers live within less than a half a mile of a stop). And more riders means more fares, helping the MTR achieve its exceptionally high ridership figures.

And although the MTR Corporation is technically a private company, it isn’t private the way Americans understand the term.

The company was formed as a statutory corporation, wholly owned by the (then colonial) government of Hong Kong. In 2000, the city partially divested, and MTR Corporate stock now trades on the open market and pays a regular dividend (though the government maintains a controlling ~75% stake).

Imagine a world where BART (or any American transit system) was so successful that it not only self-financed, but also turned a profit and remitted money back to the government. It sounds almost inconceivable.

Why the MTR makes money, and BART does not

Part of why we can’t have nice things is simply historical circumstance. Hong Kong’s topography — a group of mountainous islands with limited flat land for sprawl — meant personal automobiles were never going to scale. Also, the government of Hong Kong set the MTR Corporation up for success by granting the company land at and around each station at pre-development prices. That meant the MTR gets to internalize all of the premium they create by building out the rail line.6

BART, on the other hand, was built in the context of post-war American sprawl. Its original architects envisioned a world where workers would commute into San Francisco from peripheral suburbs, but recognized that natural chokepoints like the Bay Bridge crossing would limit the effectiveness of single-occupancy vehicles. That said, the system’s peripheries were always assumed to be lower-density communities (relative to downtown San Francisco). This model was meant to be hub-and-spoke, with no concept of maxing out development at the system’s car-dependent extremities.

Using land values to pay for transit infrastructure wasn’t a new idea, even back in the early days of BART. And although BART planners never envisioned something as vertically integrated as the Rail + Property model, they did assume they’d be able to at least partially rely on a little something called….property taxes.7

Well, we all know what they say about assumptions.

In 1978, Proposition 13 was born. Its birth cry broke the fiscal eardrums of the State of California and has left it with financial tinnitus for nearly 50 years. In less florid language, California has a longstanding system of ballot initiatives whereby voters can propose and pass changes to the state’s constitution. Once ratified via statewide plebiscite, these constitutional changes cannot be undone by the legislature and can only be removed or otherwise changed by a subsequent statewide vote. So, only a ballot initiative can defeat a ballot initiative.

The net effect of Prop 13 was to deeply constrain California’s ability to levy property taxes.8 The immediate impact on BART finances was a loss of around $32 million dollars, adjusted for inflation.9 But that one-time hit understates the longer-term impact: Without effective access to property taxes, BART has missed out on decades of real estate appreciation supported by its rail service. Instead, most of that windfall has fallen into private hands.

In 2017, BART opened the Warm Springs station. At the time, this was the southernmost extension of the system and was another step in BART’s long, slow slog into the South Bay. A later study coming out of San Jose State’s Mineta Transportation Institute measured the impact of that new station on local real estate values. The study reached two important conclusions: first, single-family homes located within two miles of the Warm Springs station saw a 9-15% increase in their property values. Second, the aggregate boost to property values within two miles of the station was over four billion dollars — that’s billion with a B. The Warm Springs extension took a little over $800 million to build, so the value the station created for nearby property owners was 5X the cost of construction.10 Put in a different way, 10% of the uplift in property values from this one station would wipe out the entire $400 million operational gap threatening service region-wide.11

So, once more for the people in the back. BART produces massive value for the region. It simply lacks an effective monetization strategy.

So where do we go from here?

As the saying goes, the first step is recognizing that we have a problem. And the core problem is that BART has a broken business model.

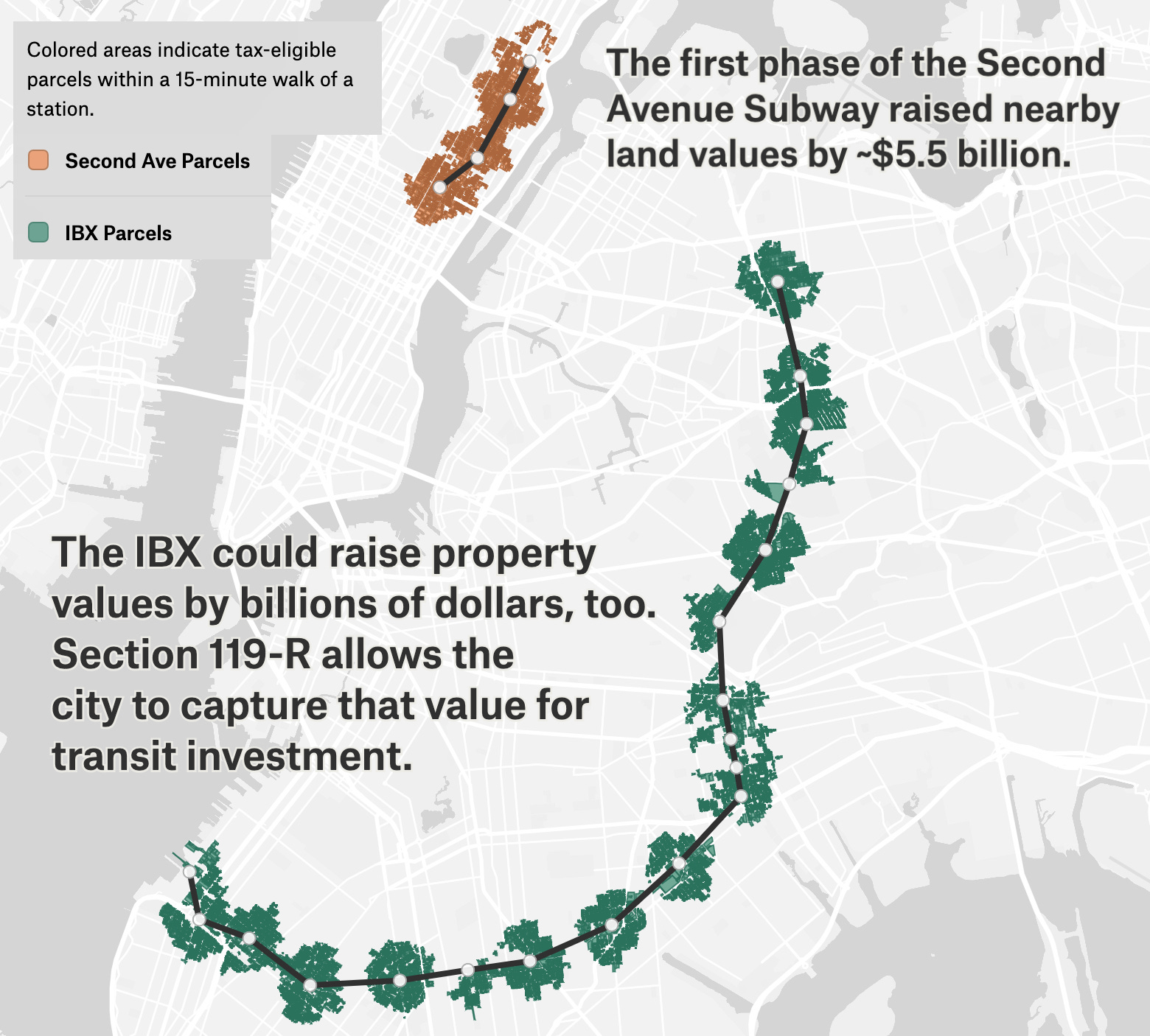

The Hong Kong MTR approach is the ideal. However, the state of California doesn’t have land to turn over to BART for development, so a second-best option would be to passively monetize the land values around its stations. That would look something like Land Value Taxation and/or TIF-Financing. This is likely how New York State will cover the long-term costs of the Interborough Express (see map below), New York City’s first rapid transit line in nearly a century. Sadly, *taps sign again* Prop 13 ruins everything. So, that’s off the table in California.

Does that mean BART remains unable to monetize the real estate value it creates and is stuck in the worst of all possible worlds?

Maybe.

In 2018, then state legislator David Chiu passed AB2923. The law granted BART de facto land-use authority over BART-owned property and required the agency to adopt transit-oriented development (TOD) zoning standards governing issues like density, height, parking, and land use.12 This was an attractive proposition given the acres and acres of surface parking next to stations across the system.

Back in 2018, I hoped this would result in something like the Rail+Property Model. Fast forward to 2026, and it’s a bit of a mixed bag.

The good news is that projects are, in fact, getting done. BART developments in Millbrae, Oakland, Pleasanton now house real-life, honest to god human beings. And many more projects are on the way. The region needs housing, so that’s good. And the TOD development pattern will help ridership.

The meh news is that these projects will generate a negligible amount of money. BART has entered into long-term ground leases, but there’s not much left after prevailing wage requirements and statutorily mandated housing subsidy targets.13

Fundamentally, AB2923 was designed to address housing policy goals, not BART’s financial needs.

What BART needs instead is a mandate to 1) develop land as a major source of revenue and 2) acquire additional properties adjacent to its stations.

Conceptually, number one is pretty straightforward. This would look like additional state legislation that gave BART the marching orders and the policy tools to turn a profit off real estate development. Number two, though, is a way to remove parcels from the control of individual municipalities (who, generally speaking, remain resistant to serious development) and put them under the purview of BART (assuming a successor version of AB2923 still afforded the agency that kind of discretion).

To be clear, passing the kind of state law I just described is not easy. Also, I’m not aware of anyone — either advocates, bureaucrats, or politicians — who is thinking about the problem in these terms. And that’s understandable. This type of plan puts BART on the right path in 10 or 20 years, but the thing everyone is focused on right now is whether voters this November will approve a sales tax increase, or if we should expect to lop off a metaphorical leg.

Taking a step back, though, I see no other path to long-term financial sustainability. BART produces value for every county it serves — value we’re capable of observing in the real estate premium it confers to property owners across the region. If we want to get serious about building a better BART, we need to be clear-eyed about the problem: BART has a broken business model; it needs a new one.

Source: Me. Come at me CalTrain-stans. (also, I know it’s actually heavy rail, but using the technically correct jargon would confuse the non-train obsessives).

Sales taxes are voter approved measures applied county-wide in Alameda, Contra Costa, and San Francisco Counties. Parcel taxes — uniform flat rate surcharges on property — have sometimes generated revenue for operational expenditure and sometimes been used to back bond issuance for larger up-front infusions of capital.

To be fair, Andrew Miller has made the case for that.

Note that this doesn’t hold true for bullet trains which are inter-regional and have economics that look more like airlines.

Yes, fellow tech folks, there’s a FLYWHEEL EFFECT.

To be precise, what the Hong Kong government sold the MTR Corp were development rights, not the land itself. The city government legally owns all land in the city and sells long term (e.g. 99-year) leases that entitle the lessee to develop said land.

At least half of you know where this is going; for those that don’t, we're about to talk about the land use policy equivalent of Tolkien’s Witch King of Angmar.

Prop 13 was a state wide ballot initiative that capped property taxes at 1% of assessed value at the time of purchase. For tax purposes, reassessment would only occur if the property changed ownership. This means that if you bought a house in San Francisco in 1978, you’re basically paying 1% on the inflation-adjusted value of what the property was worth when Jimmy Carter was President.

BART 1978 - 1979 Annual Report; page 7 (original $7million figure adjusted to current dollars).

And there’s nothing special about Warm Springs Station, either. As reported by the San Francisco Chronicle, BART’s own analysis finds an average 18% premium for property values within a ½ mile of a station for suburban East Bay Neighborhoods.

For my fellow pedants: this isn't a proposal to tax individual homeowners on their BART-conferred appreciation. If you do the math on a $1 million home, that would be like an extra $10K in yearly taxes. The point is simply that the aggregate value created by a single station extension dwarfs its construction cost — and that BART currently captures none of it. The mechanism for capture is a separate question from whether the value exists.

Technically, AB 2923 required Bay Area Rapid Transit to formulate TOD zoning standards for qualifying BART-owned land near stations and gave local governments two years to harmonize their own zoning rules with those standards. If a locality failed to do so, BART’s standards would effectively supersede inconsistent local zoning on covered BART-owned property.

AB2923 targets at least 20% of housing units developed on BART property to be subsidized affordable. After policy-goals are met, BART revenue from ground leases will be in the millions of dollars, a far cry from the structural deficit it’s facing in the $350-$400 million range.

This post reminds me of the Works in Progress article on Japan's railways. https://worksinprogress.co/issue/why-japan-has-such-good-railways/

I don't know relative political viability, but what about an alternative of the state grants the transit agency the power to auction zoning variances for a certain region around stations? No capital outlay or eminent domain problems